Adapting for dollars

How operators and investors can think about getting and climbing the ladder to meet climate adaptation finance targets

Welcome back and very belated Happy Year of the Dragon! This time of year the ultimate high holiday in my community - time with family, fireworks, lion dancing, people trying to see who received more money, fraud - so it’s always full on. I’ve also come back from some time on holiday in the Middle East to recharge the batteries - where average temperatures are rising twice as fast as much of the rest of the northern hemisphere - so it’s time to get back in the game.

There’s quite a bit of content I’ve been thinking about writing on for the next few months, but as many of you know the concept of climate adaptation as the flip side of the coin of climate security is one that is dear to me, so I want to take this month’s newsletter to focus on it in more detail, specifically taking you the interesting bits of a report on climate resilience financing by the Boston Consulting Group (BCG), Global Resilience Partnership (GRP) and US Agency for International Development (USAID). I don’t seek to cover everything - you should go in and read it yourself if you’re diving deep into this area - but I want to share the elements that caught my eye and offer some commentary for you risk professionals out there.

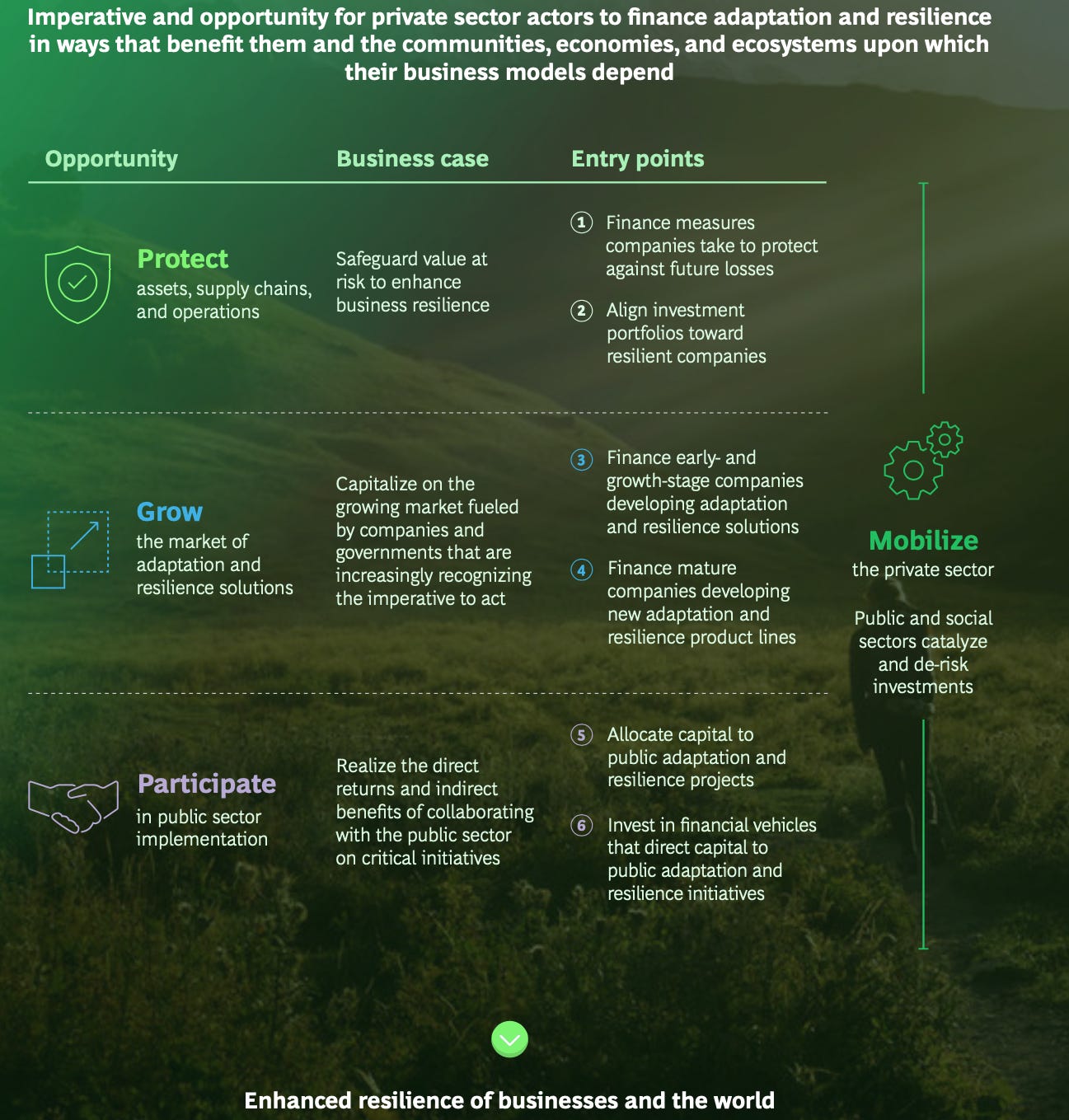

The report fundamentally breaks climate resilience finance into three pillars: Protect, Grow and Participate (all images from here credited to the authors of the report):

I think this is a fairly simple and clean way to begin to understand the value chain and where different funders / builders / operators / civil society stakeholders could assess where they may belong.

Low hanging fruit - protecting what we have

First, there is a “what’s in it for me” problem - for climate mitigation (greenhouse gas removal projects essentially), there are markets, carbon pricing (in some places) and proven funding structures. Renewable energy, charging infrastructure, metals recycling, EV manufacturing are profitable enough to pursue at scale. Adaptation as a focus for climate finance doesn’t have the same appeal today, although some existing funded projects also have an adaptation / resilience byproduct e.g. permaculture projects also benefit food security. A common refrain is “there’s no money in a seawall.”

So how do we in the commercial space get to a view of financial return on investment which includes protecting value at risk? It won’t happen overnight but putting building blocks in place through scalable success stories, timed by emergent acute crises, is necessary. I would argue that the impact of our current and near-term emissions buildup in the atmosphere (CO2 stays in the air for 300-1000 years, and it is very hard to see how carbon removal tech scales before 2030) essentially guarantees a world beyond 1.5C+ above preindustrial levels between now and 2050. So much more needs to happen on investing in people, infrastructure, and systems to prepare, survive and thrive today and into what is likely the rest of our lifetimes.

The above also makes it an attractive investment thesis because of a) predictability: high certainty of the physical risk impacts through most investors’ time horizons, b) growing consumer and business demand for solutions - whether they call it adaptation or something else - and c) it’s under-invested so much greater upside. I’d argue also d) in many countries pitching adaptation is likely to have greater political backing across political and ideological lines in representative political systems, making policy development and implementation - all else being equal - easier to enact. The MSCI / GARI report on investing in climate resilience and guiding principles for those investments, goes into even more detail about the investment thesis, growing the capital pool, the kinds of policy frameworks and investment guidelines that can be developed, and the opportunities for different kinds of investors. It’s worth a read if you want to dive into this space and see how more deeply from a finance angle how some of the security impacts we care about can drive demand for bankable solutions.

For asset managers and fellow security risk managers, the Protect opportunity is the low hanging fruit, which largely doesn’t require new untested technology to be implemented across an organisation, region or sector:

Most organisations have some form of basic enterprise risk management framework linked up with internal climate risk assessments and disclosures. Through a 2022 questionnaire by the Climate Disclosure Project, the report cites about of 40% of 18,000 companies across all sectors were already funding measures which they claim will directly improve their resilience. Investments were infrastructure (supply chain), financial (climate insurance) and operational (disaster preparedness, climate analytics). That’s good news, but it also means 60% are apparently NOT doing this. One would hope and even expect that firms in particularly vulnerable sectors (e.g. agriculture, energy, utilities) that invest heavily will build up a competitive advantage over peers, and will begin to have a material impact from a valuation perspective.

Breaking that down to incorporate climate-related and security risks, we’re looking at these acute and chronic physical threats: flooding, fire, extreme heat / cold, drought, famine. The report found that firms in almost all industries had some element of water security measure (primarily water use efficiency and storage measures), but in contrast did not do much in the way of disclosure around energy, food, health and biodiversity.

The financial cost-to-benefit ratio of these types of measures are striking:

A brief look at the methodology shows these figures are promising although it is necessarily reliant on self-declared benefits and costs. Despite the small sample sizes involved, it’s a handy reference points for investors to at least dig in deeper into the changing resilience benefits and how to extract financial value out of protecting existing assets and systems. To me, a lot of easy wins for asset managers and investors are going to be in reinforcing or adapting infrastructure with both hardware and software that are value-enhancers with existing commercial off-the-shelf tech, some of which could lead to premiums for products and services that such measures support:

sensors backed by existing technology to better anticipate risk thresholds being approached

continued $$ going into drought, heat and pest-resilient seeds, soil health (biochar, funding permaculture practice)

reducing leaking from water utilities, private water infrastructure, and other water efficiency measures for data centres, power plants, groundwater sensors. This would be quite helpful in Bengaluru right now.

Where’s the opportunity: For risk operators, I think there are a few immediate (not next year, not five years from now…today) roles we can play:

Leverage sectoral and on-the-ground expertise to a) identify and vet innovative solutions that are being thrown around your organisations to “climate problem-solve.” You know the operational reality and pain points - do the proposed tech / processes etc make sense? Is it over-engineered? How will a new project go down with the local community - which you may know much more about than the BD team back at the mothership. Are there lower-tech solutions that could work as well, or even provide a “90% answer” at a fraction of the cost? Not everything needs AI.

Enhance what and how you inform risk assessments, scenario planning and crisis management: do the models your company use to identify how they’re vulnerable to climate risk impacts incorporate the “human” or people safety element? Do the physical impacts require changes in security requirements, tools, safety equipment, physical coverage to continue to execute your mission in securing corporate assets e.g. would you advocate to install more cooling stations at your farms?

Training: if your organisation has a lot of infrastructure in low lying areas, or people working outdoors in hot climates, do you and your health and safety colleagues need to amend training and standing advice for staff and travellers?

All that takes time, people, investment and political capital. If some or much or the above aligns with your mission then there is a potential business case to invest in climate adaptation / resilience measures as a tangible corporate security initiative. The report highlights how commerciality is currently expressed with these investments: cost savings from efficiency (sounds like some solar projects I’ve seen), avoided revenue loss via continued operations, asset damage avoided via infrastructure improvements.

Making it happen: At the operational level, these may be enough to get a proposal across the line but to scale it up is still a challenge. My humble sense is that there is opportunity here for creativity to highlight in a holistic way the “how and how much” of risk reduction enables opportunity, and the number of risks that are positively reduced. I suspect that this isn’t happening enough. At the investment level, I agree with the report’s argument that more creativity is needed as the climate reality is more urgent: how debt instruments are commonly structured is not well suited for many adaptation projects, without a borrower willing to take a punt on payments for avoided harm. The report also flags a few other gaps: the lack of mature regulatory frameworks, poor or sporadic government communications to position and encourage investment in this space, and standardised methodologies for disclosure (e.g. the Institutional Investors Group on Climate Change’s Physical Climate Risk Assessment Methodology Guidelines for Integrating Climate Risk in Infrastructure Investment Appraisal is a promising one given the IIGCC’s existing respected role in the private sector coalition ecosystem). The latter I believe is a key unblocker to allow the same peer pressure effects that helped enable TCFD’s success to spill over into climate adaptation.

Growing and scaling climate adaptation as security risk measures

The Global Center for Adaptation recently estimated that of the annual US$1.3tn in overall global climate finance in 2021 and 2022, only about 5% or $63bn was for adaptation or had a significant adaptation component. That’s down from 7% of the overall climate finance pie from 2019 and 2020. The GCA report indicates flows must quadruple to just meet the needs of developing countries. At a high level, this disparity should be a rallying cry for innovation and investment…and yet we’re discussing this because there is such a long way to go.

The report highlights how business model innovation is key especially in emerging markets and developing countries - where the local needs are perhaps most acute but the socioeconomic challenges to get off the ground, let alone scale, are also the steepest. Access to funding in the right currencies, permitting, community and local government buy-in, weaning off aid / concessional grant type of funding, are just some of those hurdles.

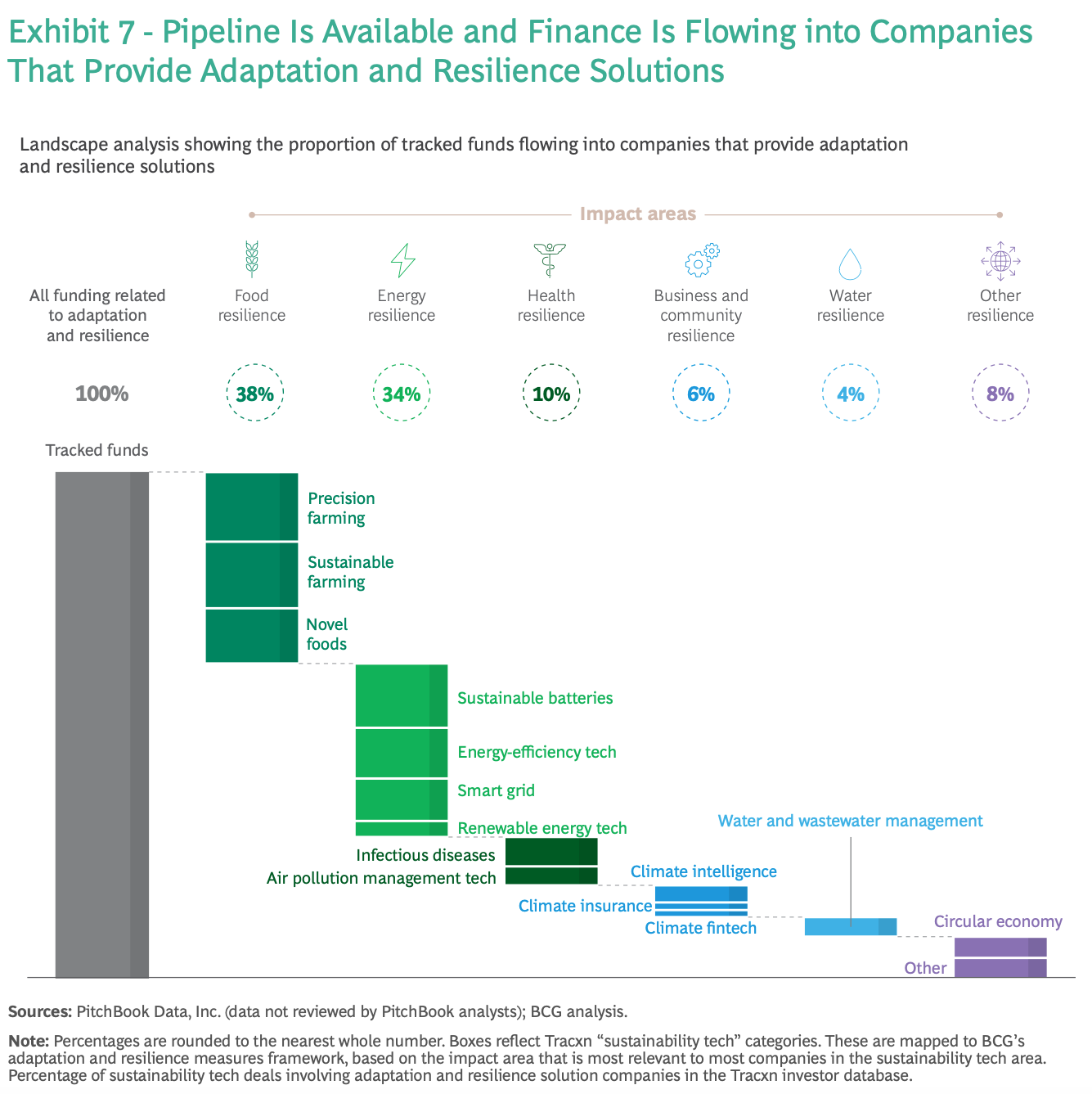

In terms of who is funding, the report focuses primarily on venture capital and private equity, where there is much greater risk appetite. The food sector dominates, followed by energy given the synergies with the growing pipeline of renewable, carbon capture and electrification projects (below). There is a suggestion that investors view adaptation and resilience solutions as essentially food and agriculture innovations. Another new study floating around in the ecosystem, by the MSCI Sustainability Institute and the Global Adaptation and Resilience Investment working group, drills down further among publicly listed companies and finds that industrials have the greatest intensity and potential in providing products and services addressing demand for adaptation and resilience.

What surprises me is that the climate intelligence / insurance / fintech pillar - much of it is software based - remains small in comparison. Given that data access and fidelity remains a massive hurdle to deploying adaptation projects given the local context that such investments demand, there should be a greater push to invest in the data and intel side of this. Mitiga, ClimateX, and a host of other startups are vying for this space, alongside a bevy of consultancies ranging from specialist houses to the Big 4, so I’m confident that we may be underestimating the amount and momentum of capital flows here - likely from undercounting the host of mitigation-driven startups and solutions. I would be particularly keen to see those smartly blending software and hardware e.g. leveraging existing telco infrastructure to deliver greater capture of risk data at a hyperlocal level.

The report further highlights that good local startups know their market, and valuation multiples are generally strong. However, there appears to be a knowledge gap - a lack of awareness from investors and government stakeholders alike of climate risks’ ripple effects which then leads to underestimating the commercial value of adaptation technologies.

This is a space where I think there is a more limited role for most corporate security / risk folk given the operational nature of so many teams. But teams with a track record of due diligence work could see opportunity in vetting their firms’ potential investments in intelligence and remote sensing technologies. Or, bolt-on security-additive solutions onto existing infrastructure / capital projects that provide a demonstrated cost savings (e.g. lowering insurance costs) or enhancement of products (e.g. service uptime) over time. Our experience and insights, in the right setting, is itself an innovation point to help make a solution more attractive / less risky.

This may also be one avenue to bring greater alignment between a corporate intelligence team with an organisation’s broader business intelligence / analytics / corporate development functions. The advantage for security / intel folks is we know how to integrate information from our people networks with our other open sources to bring actionable insights in a way that is often unique to an organisation. Applying elements of that model elsewhere could amplify such a team’s strategic impact and value. Carve-out for folks in the insurance space, who have a golden opportunity to take a more proactive role in enhancing your firm’s cutting edge climate risk mitigation products and consulting services.

For governments, international NGOs and bodies like the UN, however, there is. a massive an urgent opportunity: to invest and deploy solutions at scale to adapt critical military infrastructure to a range of acute and chronic weather conditions, recognising that “things have. to work” across a broader tolerance range than before. That’s where having programmes that parallel DOE loans programme for energy transition, but for national defence, can be a game-changer for startups and scale-ups. For funders, government clients can - and have - significantly brought down costs which can enable innovation outside of the government / national defence space. John Conger’s recent piece on the US National Defense Authorization Act highlights some of these changes and challenges.

Getting involved: so what do our jobs look like 5 years from now?

Why should I care? First: time flies. Second: what you invest in yourself, your team or organisation today is likely to pay dividends only over time. Remember that a decade ago everyone was climbing over each other trying to learn about “cyber,” and 5-10 years before that, everyone scrambled to become a “terrorism expert.” The security industry is heavily influenced by external trends over which it has adapted to - sometimes quickly, often reactively and belatedly. What happens to the mix of focus and expertise for corporate security / intel teams in a much hotter world with more acute weather events is a discussion for the pub or cafe, but I’m confident that won’t be the same mix as we see in many corporates today. Wouldn’t you want to get ahead of the next thing (hint: climate and AI) so that when it really hits hard - and it is a today problem in some regions already - you’re ready to take advantage for the benefit of your organisation, investment and career.

Links and cool stuff catching my eye this month:

How can climate resilience be ‘inclusive’ at the municipal level? - Observer Research Foundation

Research uncovers reason for mass migration: ‘There’s more to the story’ - The Cool Down

Climate Change, Conflict and (In)Security: Hot War, edited by Tim Clack, Ziya Meral and Louise Selisny. Insecurity Clack and Meral. It’s sitting in my study, and looking forward to reading through.

See ya next time!